The S&P 500 rose more than 10% over the last 12 trading days, reaching new highs above 7000 as risk sentiment returned to markets after the US and Iran agreed on a two-week ceasefire with negotiations for a permanent end to the war currently ongoing. Asian equity markets reacted in the same way, with the Nikkei 225 and Taiwan Stock Index all hitting new highs as well. Brent crude oil prices have now dropped to sub-100 levels, with the DXY US Dollar Index also falling back to pre-war lows.

One of the biggest indicators of market sentiment, the VIX volatility index has dropped from market-panic levels above 30 to below 20 in the same timeframe, showing that investors are no longer pricing in huge market moving events arising from the conflict. In other words, a full resolution to the conflict is expected by investors, with little re-escalation.

However, this rally is not easily rationalized. Many obstacles are still present in negotiations, with the US and Iran refusing to back down on key points like the enrichment of uranium and control over the Strait of Hormuz. Furthermore, despite the truce, oil flows remain heavily constrained in the Gulf, even with Iran’s recent announcement that the Strait of Hormuz would be “completely open” for the duration of the Lebanon ceasefire. Notably, central banks around the world have turned more hawkish than before the war, with less rate cuts, and even rate hikes now projected for 2026.

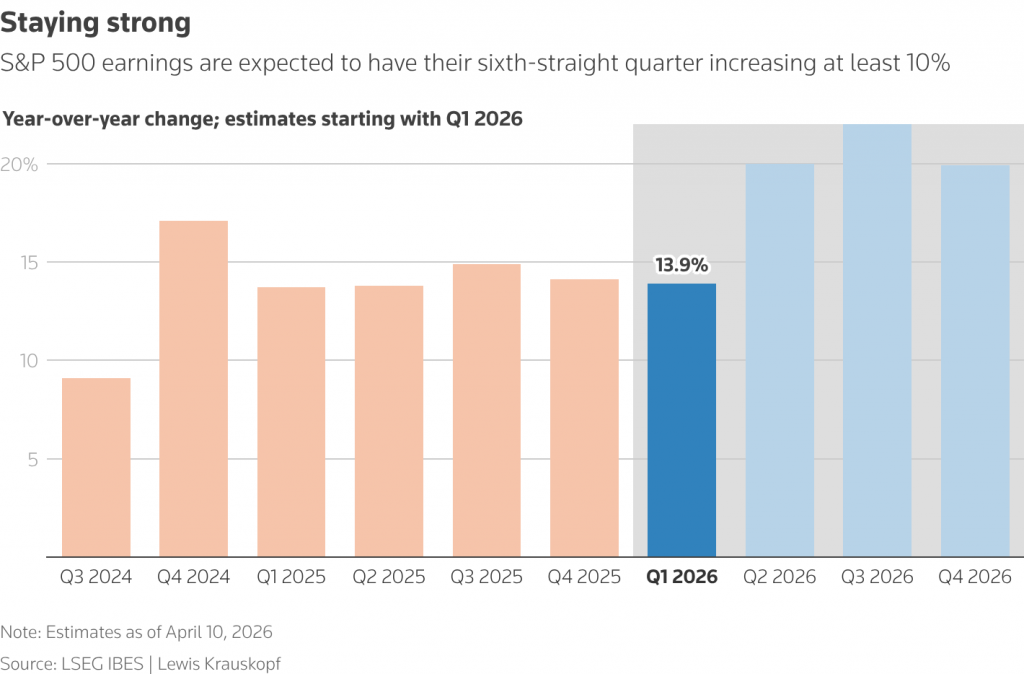

Record-breaking earnings from US banks profiting off the increased volatility, as well as continued exceptional growth in AI related stocks have also contributed to the stock market’s recent rally. Estimates from LSEG IBES also show that S&P 500 companies are expected to increase earnings by 19% in 2026 compared to 15% from before the war. But with much uncertainty surrounding the oil shock resulting from the conflict, there is reason to believe that earnings outlook have not fully priced in the potential effects on inflation and interest rates.

In the near term, the S&P 500 is approaching overbought levels according to the Relative Strength Index (RSI), climbing above the 70 level, with a potential pullback perhaps on the cards. Markets will likely continue to trade off headlines in US-Iran negotiations, though it remains difficult to explain how markets are essentially pricing in a better outlook now than when before the war began.