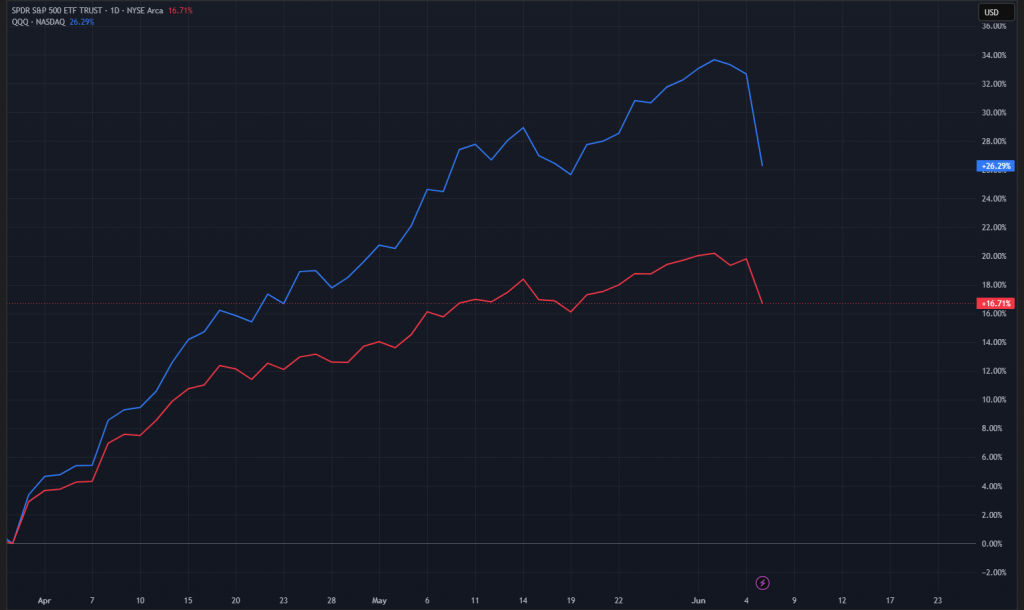

Markets finally took a breather on Friday from the non-stop rally over the past few weeks, with the S&P 500 down 2.64% while the tech-heavy Nasdaq Index plummeted nearly 5%. The reason? Non-farm Payrolls (NFP) data for the month showed an increase of 172k employed in May, well-above the market expectations of 85k, displaying the continued resilience of the American economy despite the ongoing conflict in Iran.

But how does this make sense?

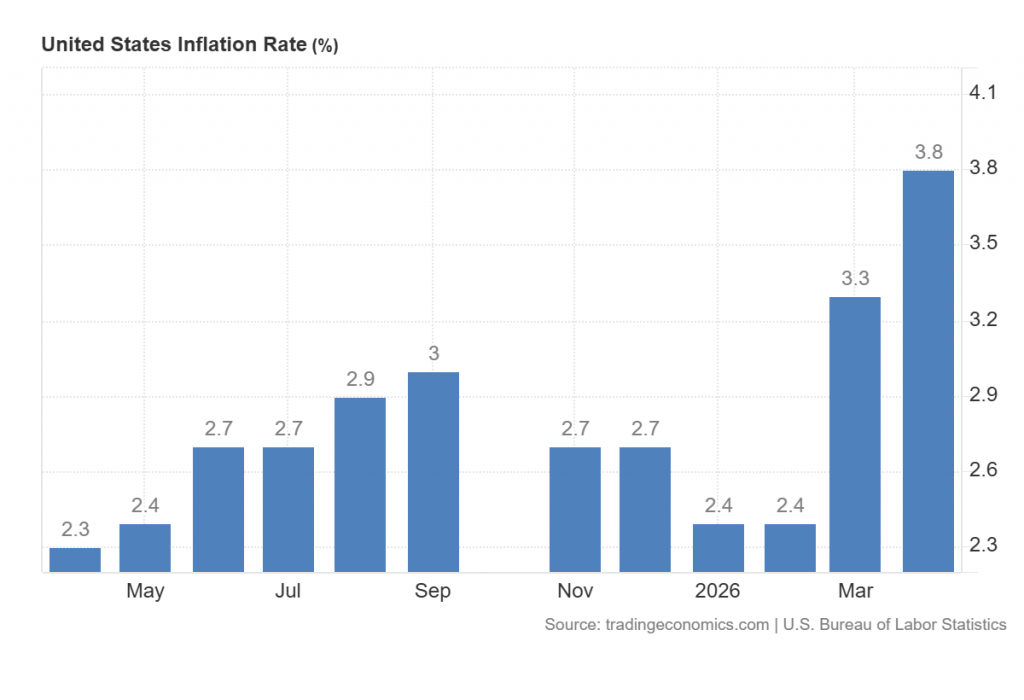

Going back to my previous post, we have seen how the energy crisis has been pushing inflation higher, to the point where odds were around 50/50 on whether the Fed would hike or keep rates steady throughout the year. Besides inflation, the threat of higher energy prices was expected to weigh on company margins and growth, but the strong employment numbers have now dispelled those fears.

Instead, markets are now worried that the persistent strength of the economy could potentially incentivise the Fed to hike rates to keep inflation in check, which has been rising ever since the start of the war.

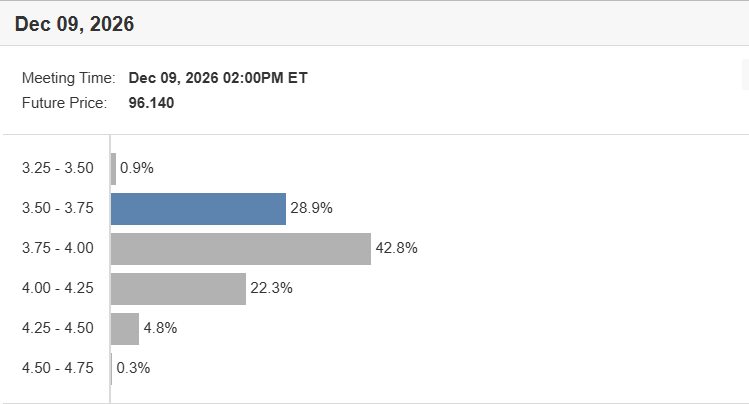

After the jobs report, the balance has shifted more decidedly towards rate hikes, increasing to a 70% chance of at least 1 rate by the end of the year. An increase in rates makes the cost of borrowing for companies higher, which disproportionately hit small caps that rely heavily on debt financing. It would also make the cost of financing the unprecedented amounts of capital expenditures on AI from tech stocks more costly, which partially explains the large losses in the Nasdaq on Friday.

Besides this, Broadcom’s (ticker AVGO) earnings result where guidance failed to meet forecasts poked holes in the AI optimism trade that has been carrying markets, showing just how high expectations are now.

However, in my opinion, the employment data was just an excuse for markets to rotate out of the biggest winners in sectors where positioning has been concentrated. With the incredible run-up that equities have been having in recent months, it’s not crazy and maybe even healthy to have some profit-taking and selling to balance it out. A bad employment report would have just as likely sent markets down too, but with the narrative of economic strain and stagflation instead.

Negotiations between Iran and the US have continued to stall, and potentially worsen with both sides striking each other in recent weeks. But looking at Trump’s comments downplaying the events suggest he’s done with the conflict, and I expect the status quo to remain. Shipping through the Strait of Hormuz have once again dropped off after a brief recovery, though oil prices have fallen as fears over a restart in the conflict have subsided.

Going forward, I believe attention has shifted away from the Iran conflict and towards inflation and interest rates instead. To this end, the upcoming CPI inflation report on Wednesday, June 10 is going to be key to determine whether the sell-off on Friday was just occasional profit-taking, or a sign of more pain to come.

Investment Outlook

(CPI – Lower than expected)

Equities: Bullish

Bonds: Bullish

Gold: Bullish

Oil: Neutral

(CPI – Higher than expected)

Equities: Bearish

Bonds: Bearish

Gold: Bearish

Oil: Neutral