In the recent few weeks, US equity markets have hit all-time-highs after all-time-highs, with the S&P 500 index hitting the 7,500 mark just this Thursday, before a bond market selloff and profit taking on Friday pared gains. The rally came about amid a wave of optimism over a potential resolution to the Iran conflict together with the highly anticipated Trump-Xi summit that just concluded.

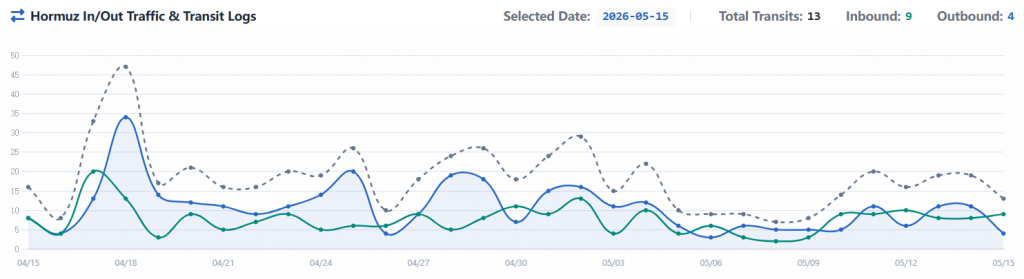

On the Iran conflict, markets seem to be experiencing headline fatigue, with little material progress made since our last post despite claims from President Trump. The Strait of Hormuz remains heavily restricted with daily ship transits having plateaud to around 20/day, as oil prices climbed back near previous highs.

However, the pressure from the US blockade is starting to be felt by Iran, with research from Kpler suggesting oil storage space could run out within a month as Iranian tankers struggle to make it through. Oil is one of Iran’s key exports, and revenues from the commodity are estimated to make up 25-30% of the state’s budget, and 9% of its GDP. Trump hopes the financial pressure would drive Iran to accept some of his peace terms, though hardliners within the IRGC continue to dismiss them.

On the Trump Xi-summit in China where many CEOs of US companies followed Trump for trade discussions, the meeting initially appeared to be more constructive. Both Presidents were exchanging positive comments throughout, where Trump claimed “fantastic trade deals” were made. Aside from purchases of Boeing jets and unconfirmed claims to purchase US farm goods, nothing much was achieved with no substantial deal being struck to normalize trade between the two countries. The topic of Iran was also brought up, and while both presidents agreed that the strait should be opened, no indication of a change in China’s policy took place.

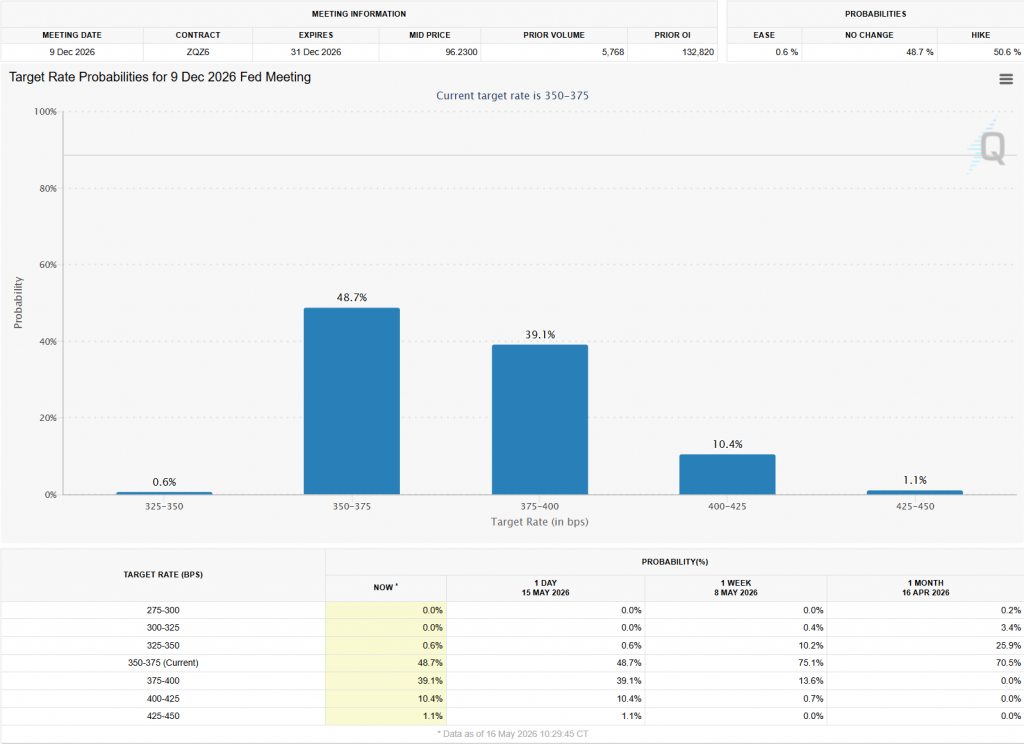

Turning to the economy, US Treasury yields have been rising across the curve with 30 Year Yields climbing above 5% as inflation worries triggered a global selloff in bonds that spread to the equity markets on Friday. Wholesale inflation in particular surged 6% against estimates of 4.9% year-on-year. As a result, hopes of a rate cut by end of 2026 have all but vanished with markets now pricing in a 50% chance of a rate hike, a stark contrast from a month ago.

So what does this mean for the week ahead? I expect oil to remain around current levels as US and Iran remain stuck over the status quo. Worsening inflation numbers and increased rate hike expectations are likely to continue to weigh on bonds, while rising yields make holding gold less attractive. Equities have been rallying non-stop the past few weeks, and certainly seem ripe for a pullback amid the macro backdrop, though timing will prove difficult.

Investment Outlook

Equities: Slightly Bearish

Bonds: Bearish

Gold: Bearish

Oil: Neutral